What is a 1031 Tax Exchange?

As an investor, it’s important to stay sharp on the facts when considering any changes to your investment portfolio. One of the smartest moves you can make is to structure a 1031 Tax Exchange. In this article, INCO Commercial reviews the details of a 1031 Exchange and how it can benefit you.

The 1031 Tax Exchange, also known as a ‘Starker Exchange,’ allows an investor to sell a property and reinvest the proceeds in a new property. In doing so, all taxes on capital gains are deferred. The official wording states:

“No gain or loss shall be recognized on the exchange of property held for productive use in a trade or business or for investment, if such property is exchanged solely for property of like-kind which is to be held either for productive use in a trade or business or for investment.”

A delayed 1031 Tax Exchange occurs when the exchangor relinquishes his property before acquiring new property. The property the exchangor owns is first transferred, then the property the exchangor wishes to own is acquired second.

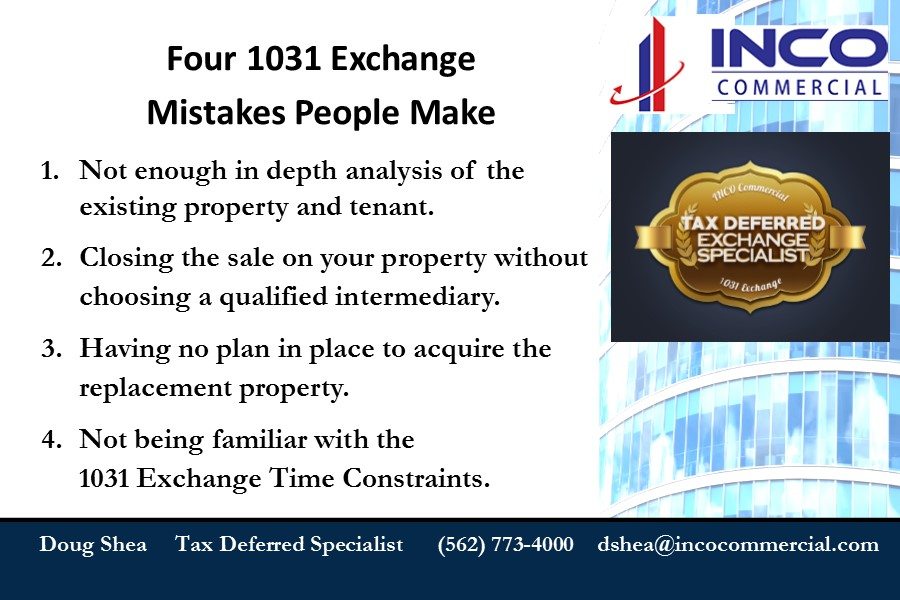

A successful exchange requires strict adherence to the guidelines outlined within the tax code.

There are four basic requirements when entering into a delayed exchange. It is crucial to review these under the counsel of a tax accountant or attorney to guarantee proper adherence to the tax code. INCO Commercial is ready to help you make arrangements and assist you each step of the way.

Property Qualifications

The internal revenue code requires that the properties involved in an exchange must be held for productive use in trade or business or for investment, and they must be “like-kind”.

Like-kind simply means that if two assets or properties are considered the same type, an exchange between them would be tax-free. However, the like-kind requirement is often a source of confusion for investors. All real estate is technically like-kind, with the exception of property outside the United States. For example, an investor selling a rental home in the U.S. can exchange into a multi-plex, provided that it is also located in the U.S. Similarly, an investor selling a warehouse can exchange into a percentage interest in an office building. However, the line is drawn with dealer properties, which are ineligible for a tax exchange.

A dealer property, or property held as inventory, is one purchased with the intent of “flipping,” or turning around quickly. While most real estate purchases are considered “investments,” the IRS makes the final determination whether the property is a longer-term investment or a dealer property.

The most important factor in determining whether a property is dealer property or not is “intent”. Upon an audit, the IRS will carefully examine what the investor intended to do with the property at the time of acquisition. This can include a review of the type of mortgage, what kinds of improvements were made, correspondence relating to the property, the type of insurance coverage, etc. If the IRS determines that the intent of the investor was to quickly resell the property, it could be considered dealer property and thus ineligible for exchange.

Timeline

The IRS provides a maximum of 180 days to complete an exchange. The timeline begins upon the close of escrow (COE) of the relinquished property. The replacement property (or properties) must be acquired on or before midnight of the 180th day; there are no exceptions. Additionally, the IRS requires that all potential replacement properties be identified by midnight of the 45th day.

If the replacement property/ies can not be acquired on or before day 180, the exchange is null and taxes must be paid.

Identification Rules

Identification of all potential replacement property is required on day 45 of the exchange. Identification must be in writing and the description of the properties must be unambiguous. The IRS provides two rules for identifying replacement property:

- The 3 Property Rule – The 3 Property Rule allows for identification of any three properties of any price anywhere in the United States.

- The 200% Rule – The 200% Rule is an option for identifying more than three properties. With the 200% Rule, four or more properties can be identified, however the combined value of all properties identified can not exceed 200% of the property sold. For example:

- Investor sells a rental home for $500,000. Investor can identify ten $100,000 rentals, five $200,000 rentals or any combination of properties, provided the aggregate value does not exceed $1,000,000.

Tax Deferral Requirements

To defer 100% of the capital gains tax liability, two requirements must be met:

- Reinvest all the cash generated from the sale of the relinquished property

- Purchase property equal or greater in value to the relinquished property.

The two requirements listed above can be accomplished in a variety of ways. For example, an investor selling a $500,000 rental, with $200,000 in equity, can purchase two $300,000 properties with a $100,000 down payment on each.

A partial exchange is also possible. This can occur in a trade down situation, where the replacement property is of less value than the relinquished property (i.e. sell for $500,000, buy for $400,000). A partial exchange will result in a partial deferment of the tax liability. Some, but not all of the taxes will be owed.

Property-related tax management can be a daunting task, especially with the strict code enforcement. Having a strong team with years of industry experience is not only crucial, but can relieve some of the stress on your end.

INCO Commercial is committed to ensuring our clients accomplish their objectives through our quality commercial real estate brokerage and advisory services. Explore our website, visit our contact page, you can reach out to Doug Shea at 562-773-4000 for immediate assistance.